Everyone has ideas. Some of them may be worth running with, while others are probably not so good.

However, even if your project looks awesome on paper, there’s a big difference between that and creating a successful startup company.

Do you have what it takes to be an entrepreneur?

If your answer is yes, then you need a detailed guide on how to start a startup.

For those of you who haven’t launched a business before, it can sound like an intimidating task.

Don’t get me wrong – I’m not saying that getting your startup off the ground is an easy mission.

It takes hard work, dedication, money, some sleepless nights, and, yes, some failures before you succeed.

Nearly 20 percent of businesses fail in the first year, and just because you make it beyond 12 months doesn’t mean your startup is going to continue to thrive.

According to government stats, 30.6 percent of businesses fail after their second year, 49.7 percent fail after five years, and 65.6 percent fail after their tenth year.

Once you get your company off the ground, it doesn’t get any easier: you need to work just as hard to keep it going each year.

With that said, it’s useful to have a guide and a set of instructions to follow to learn how to launch a startup.

When I write about launching a startup, I’m talking from personal experience. I’ve created several startup companies like Crazy Egg, Hello Bar, and NP Digital.

I’m happy to share my knowledge and experience to help make things a little easier and less stressful for you as you go through this process.

Realistically, it takes hundreds of stages to launch your company, but I’ve narrowed down the top 7 steps into a blueprint for you to follow if you want to learn how to start a startup and learn how to create and develop your own business.

In the following article, I outline and discuss each step in detail so you have a better understanding of what I’m talking about.

Let’s begin with the basics.

1. Create a Business Plan

Have you heard the saying ‘if you fail to plan, you plan to fail?’ That was the thinking of Founding Father Benjamin Franklin.

Well, research appears to back that up. Study after study shows that businesses with a plan are more likely to succeed. In addition, you can find many articles spelling out the importance of a business plan.

However, the Small Business Development Center at Duquesne University explains it most succinctly:

“A business plan is a very important and strategic tool for entrepreneurs. A good business plan not only helps entrepreneurs focus on the specific steps necessary for them to make business ideas succeed, but it also helps them to achieve short-term and long-term objectives.”

It’s pretty straightforward, really. Having an idea is one thing, but having a legitimate business plan is another story.

A proper business plan gives you a significant advantage, but what should you include in a business plan? It helps if you think of it as a written description of your company’s future. Basically, you outline what you want to do and how you plan to do it.

Typically, these plans outline the first three to five years of your business strategy and detail your business’s purpose and aims. Ideally, your document should outline your business goals, strategies, and your plans for achieving them.

Here are the key steps to writing a successful business plan:

- Outline your business goals

- Describe your target market

- Explain your product or service

- Detail your marketing and sales strategies

- Write down your financial projections and detail the funding

- Summarize your overall strategy

If you need some help with your plan, the Small Business Administration has an easy-to-follow guide, along with some templates.

2. Secure Appropriate Funding

Without adequate funding, your business won’t launch or stay afloat long-term. According to Statista, in 2021, there were nearly 840,000 businesses that had been in operation for less than a year. Many of these startups won’t survive because they underestimate the cost of doing business.

Perhaps you’re wondering what level of financing you need? When it comes to raising cash, there’s no magic number that applies to all businesses. The startup costs vary from industry to industry, so your company may require more or less funding depending on the situation.

Costs also vary depending on whether you’re a brick-and-mortar store, e-commerce enterprise, or service business. If you’re unsure how much you might need, try the SBA’S startup cost templates to get a better idea.

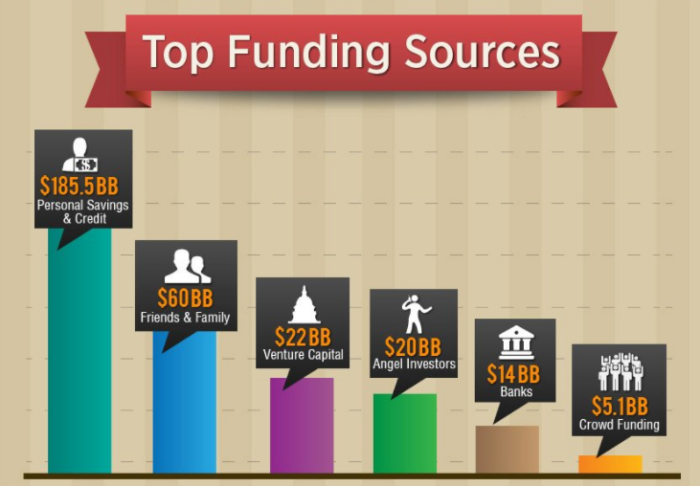

Once you’ve got a clearer picture of the costs, where do you get the funding? These days, most startups get their funding from:

- Online startup loans, which you can apply for online and pay back over time, with interest.

- SBA microloans, providing up to $50,000 in loans for start-up businesses. The main advantage is the lower interest rates.

- Lines of credit, which is a type of loan available in both secured and unsecured formats.

- Invoice factoring/financing, a process in which a business sells its invoices to a third party, at a discount.

- Friends/family/personal loans, which are unsecured loans.

- Business loans, which you pay back over an agreed period.

- Angel investors, who have considerable wealth and give seed funding to start-up businesses.

- Crowdfunding, where you raise money from a group of investors online.

Let’s circle back to our business plan for a minute.

All business plans contain a financial plan. This usually includes a:

- Balance sheet, which displays your business’s assets, liabilities, and owner’s equity of the company.

- Sales forecast, which predicts future sales.

- Profit and loss statement, which details your earning and spending patterns. This figure helps calculate your net income.

- Cash-flow statement, or financial statement detailing how much your business has spent and generated.

You use these financial statements to determine how much funding you need to launch successfully. Additionally, you may discover that the number is significantly higher than you originally anticipated.

For example, I’m sure you’ve heard someone say, “That would make a great app,” or “I should make an app for this.”

Do you know how much it costs to make an app? Depending on the complexity, you’re looking at anything between $40,000 – $300,000, and that’s just to make it.

It doesn’t include the cost of running it or customer acquisition costs.

This is the point I’m making: to secure the appropriate funding, you need to find out how much money you need.

To find this number, you must research and predict realistic financials in your business plan.

Let’s say you discover that your startup needs $100,000 to get off the ground.

What if you don’t have $100,000?

You’ve got some options, like bank loans and commercial lenders, and that’s the way many small businesses go. With this said, banks are less likely to give large amounts of money to new companies with no income or assets to default on, which may make it hard for your typical startup to get the funding they need.

Don’t worry, your dream isn’t dead yet. You can find investors. They could be:

- Friends

- Family

- Angel investors

- Venture capitalists

- Crowdfunding

However, whichever method you use, proceed carefully because you don’t want to start giving away significant equity in your company before you launch.

Then, if you get lucky and find a potential investor, you need to know how to pitch your idea quickly and effectively. Here are some tips to help you do that:

- Memorize your financial numbers; ensure you know them inside out.

- Refer to your business plan and ensure your financial figures cover the costs.

- Make sure your business plan is presentable so you can give potential investors a copy.

- Practice and perfect your pitch.

One more thing: It’s imperative that your business plan has a proper executive summary to entice busy investors.

Once you secure the appropriate funding, you can proceed to the next step of how to start a startup business: finding the right people.

3. Surround Yourself With the Right People

No one makes it on their own. William Proctor might not have been a high-profile, successful businessman if he hadn’t met James Gamble.

Where would we go for advice if Larry Page hadn’t met Sergey Brin? Not Google, that’s for sure.

Then what if Ben Cohen never met Jerry Greenfield? We would’ve been denied one of the world’s most famous ice cream brands.

Even if you’ve already got a co-founder in place, you need some core staff.

Where do you start? According to Business News Daily, there are eight people your startup needs:

- CEO and COO. Between them, they develop a vision and put it into action.

- Product Manager, who is responsible for taking a product from its development stages and onto the market.

- Chief Technology Officer, who works with executive members to oversee the technical side of a business.

- Chief Marketing Officer, whose job involves creating a marketing strategy and executing it.

- Sales Manager, for managing customer relationships, selling products/service, and motivating the team.

- Chief Finance Officer, who manages the financial planning and decisions for a company.

- Business Development Officer. This is a varied role that involves drawing up a business plan, establishing funding, and building customer/relationship funding.

- Customer Service Officer, who assists customers with their questions, any complaints, and providing product information.

However, your business structure depends on the industry, so look at the above as definitive.

When you’re just starting up, hiring an entire team often isn’t realistic, and you find yourself wearing several business hats. That’s OK, to an extent. Just remember to play to your strengths and outsource if you can’t afford to recruit.

That said, there are some experts you should consider essential, including a:

- Lawyer

- Accountant

- Financial advisor

Unless you’re an expert in law, finances, and accounting, these three people can help save your business some money in the long run.

They can explain the legal requirements and tax obligations based on how you structure your business. For example, it could be a:

- Sole proprietorship

- Partnership

- Corporation

- Limited liability company

While your lawyer, accountant, and financial advisors are not necessarily employees on your payroll, they are still important people to surround yourself with.

Finally, for this section, don’t forget the fundamentals for starting any company:

- Register your business name.

- Get a federal ID number from the IRS. The IRS lets you submit your business information online to get your employer identification number (EIN).

- Get insured: Shop around and find an insurance agent who can get you plenty of coverage at an affordable rate.

Now that you’ve got staff, you need to start work on a website and find a place to base your business.

4. Find a Location and Build a Website

Now you’re ready for the next stage of your how-to start a startup plan: finding a physical location and setting up a website.

Whether it’s offices, retail space, or a manufacturing location, you need to buy or lease a property to operate your business.

Unless you’re working from a home office, your two main options are leasing or ownership. Leasing usually works as out more expensive long term; however, don’t just base your decision on costs. Leasing and ownership both have their pros and cons. Look at the whole picture before making a decision.

I appreciate that it may not be realistic for all entrepreneurs to tie up the majority of their capital in real estate.

Strategize for this in your business plan and try to secure enough funding so that you can afford to buy property. It’s worth the investment and can save you money in the long run.

Let’s move on to setting up a website.

Today, your company can’t survive without an online presence. Don’t wait until the day your business officially launches to get your website off the ground, either, and remember, it’s never too early to start promoting your business.

If customers are searching online for a service in your industry, you want them to know that you exist, even if you’re not quite open for business yet.

The beauty of an online presence is you can even start generating some income through your website before you find premises. If it’s applicable, start taking some pre-orders and scheduling appointments.

For those of you who aren’t convinced about the pre-orders business model, many startups are succeeding with it.

Here are some tips about how to launch and promote a successful website:

- When designing a website, it is important to keep the user in mind. The layout of the website should be easy to navigate and use. The colors and fonts should be easy on the eyes.

- Make your website visually appealing. Use eye-catching images and dynamic designs to make the website stand out from the competition.

- Keep the content of the website fresh and up-to-date to keep users coming back to visit your site. Your website is an ideal place to keep your audience up-to-date with a glimpse inside your company, product launches, and, of course, the details of your business premises.

- Another important thing to keep in mind is usability. Your site should be easy to use on all devices, from desktop computers to smartphones and tablets.

Finally, make sure that your website is fast.

I can’t stress this point enough.

I’ve got a video tutorial that explains how to speed up your website.

All of these items combined may sound tough, but it’s really not that difficult. Just focus on one task at a time, and you’ll get there.

Once your website is up and running, you need to expand your digital presence. To do this, use social media platforms like:

- TikTok

- Snapchat

Your prospective customers are using these platforms, so you need to be on them, too. However, when choosing a platform, ensure you go where your core audience is. For instance, if you’re targeting a younger market, TikTok may be ideal.

5. Become a Marketing Expert

If you’re not a marketing expert, you need to become one.

You might have the best product or service in the world, but if nobody knows about it, then your startup can’t succeed.

To start spreading the word, you must learn how to use digital marketing techniques like:

- Content marketing

- Affiliate marketing

- Email marketing

- Search engine optimization (SEO)

- Social media marketing (SMM)

- Search engine marketing (SEM)

- Pay-per-click advertising (PPC)

However, if you’re starting a small business in a local community, some of the traditional methods can still work well. Think:

- Print advertising

- Radio advertisements

- Television

- Billboards

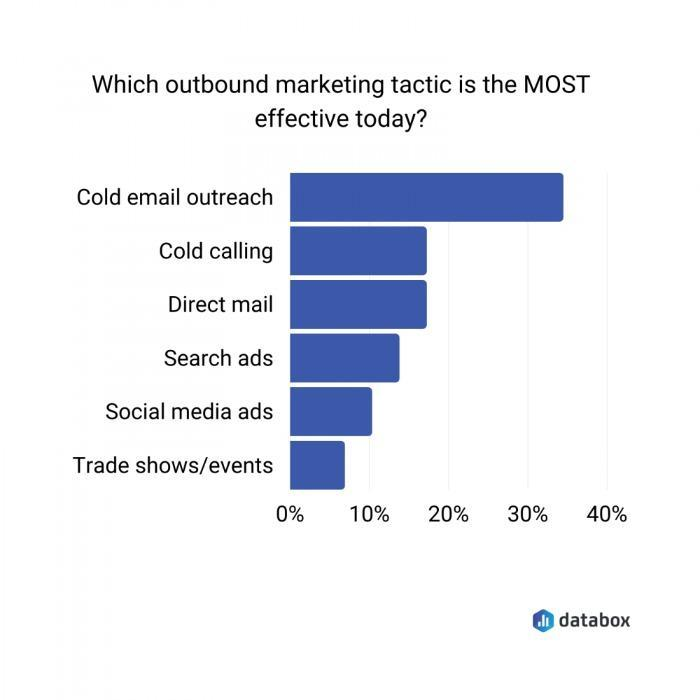

While some would argue that outbound marketing efforts are not as effective these days, research shows that methods like cold emailing and calling still work well.

For those of you who aren’t efficient marketers, there is no shame in hiring a marketing director or even a marketing team, depending on the size of your company.

Your marketing efforts will be one of the most important, if not the most important, components of launching your startup business. To improve your chances of success:

- Allocate a marketing budget.

- Determine how you’re going to distribute this money across different channels.

- Have a plan and try to maximize your return on investment for each campaign.

Take these numbers into consideration before you spend your entire budget on something like banner ads.

The bottom line is this: Marketing needs to be a top priority for your startup company.

6. Build a Customer Base

If you’re following this plan in order, the good news is that you’re already on the right track to building a customer base.

Starting a website, growing your digital presence, and becoming an effective marketer are all steps in the right direction. However, now it’s time to put these efforts to the test. That means:

- Opening your doors (or website) for business.

- Getting a customer to make a purchase is the first step.

- Retaining customers.

There are three keys to customer retention:

- Customer service

- Customer service

- Customer service

It’s no secret. The customer needs to be your main priority. They are the lifelines of your business, and they need to be treated accordingly.

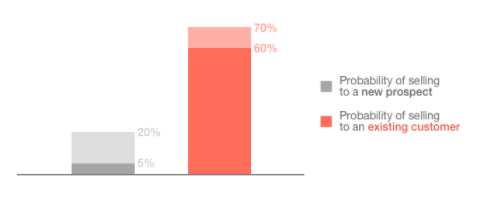

Once you establish a steady customer base, you can use it to your advantage.

You’ll get more money from your existing customers than from new ones.

It’s a more effective method than cross-selling.

Less than 0.5% of customers respond to cross-selling.

Over 4% of your customers will buy an upsell.

These strategies both double back to having effective marketing campaigns.

Overall, establishing, building, and maintaining a customer base will help you get your startup company off the ground.

7. Prepare for Anything

Expect the unexpected.

Launching your startup company won’t be easy, and you need to plan for some hurdles along the way.

Don’t let these speed bumps become roadblocks.

You can’t get discouraged when something goes wrong.

Preserve and push through it.

The difficulties that you face while launching your startup company help prepare you for the tough road ahead.

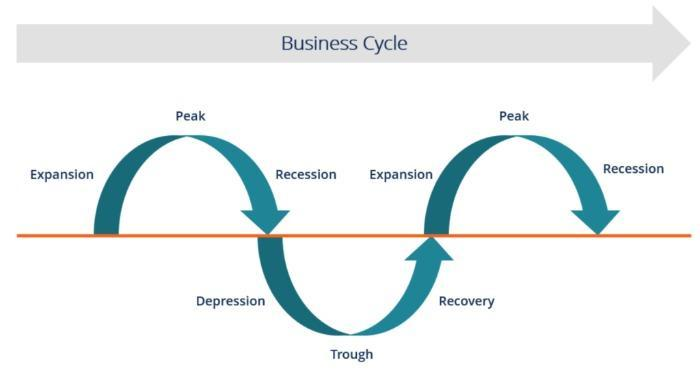

Even after your business is up and running, it won’t necessarily be smooth sailing for the entire lifecycle of your company.

As illustrated above, you face peaks and valleys while your company operates.

Mistakes and setbacks happen.

Some of these things will be out of your control, like a natural disaster or a crisis with the nation’s economy.

Employees will come and go.

You’ll face tough decisions and crossroads.

Sometimes, you’ll even make the wrong decision.

That’s OK.

Part of being an entrepreneur is learning from your mistakes.

It’s important to recognize when you’ve done something wrong, move forward, and try your best to make sure it doesn’t happen again.

Pay your bills.

Pay your taxes.

Operate within the confines of the law.

As long as you’re doing these things, you’ll be able to fight through any obstacle your startup company faces in the future.

FAQs

Check if your idea is viable. Do some research and ask around. Are people looking for a business/service like yours? Then ask yourself: How are other businesses in your sector performing? Have you spotted a genuine gap in the market?

Then you’re ready to start drawing up a business plan.

There are several sources, including personal financing, banks, crowdfunding, friends, family, angel investors, and venture capitalists.

In the vast majority of cases, yes. You also need a social media presence that is applicable to your audience. After all, social media is a free, efficient way to reach a huge volume of people that you couldn’t otherwise target.

It depends on your budget. Begin with strategies like social media, free press release distribution, and content marketing. As your business grows, you can allocate a budget for affiliates, email marketing, SEO, online ads, and influencer campaigns.

Conclusion

Let’s recap.

Launching a startup company is not easy.

First, you need to determine if your idea is worth turning into a business, then you must determine if you have what it takes to become an entrepreneur.

The percentage of entrepreneurs in the United States is growing strong, and each one of them is going to face challenges along the way.

With that said, having a proper blueprint to follow helps simplify the process. You can get learn the basics of how to start a startup by following the seven steps, and adapting them to suit your individual needs.

With that said, most successful businesses start with validating an idea, creating a comprehensive business plan, and raising adequate funding. Without proper financial planning, your startup doesn’t stand a chance.

Then, surround yourself with the right people and play to your strengths.

For instance, if you’re great at organizing and motivating, focus on that; If marketing just isn’t you, outsource it to a professional who excels in that area.

Don’t forget about lawyers, insurance agents, and accountants to keep your business in order, and make sure you have essentials like an online presence.

Launching your startup is an imperfect journey, and you must prepare for unforeseen circumstances. However, proper planning and execution help limit these hurdles and get your business off to a flying start.

How will you raise funding to get your startup company off the ground?